Managed Care Contracting - Everything Providers Need to Know in 2026

Complete guide to managed care contracting for healthcare providers. Understand contract types, essential components, payment models, and common challenges in 2026.

Cameron Fletcher

Head of Growth at PayerPrice

Understanding managed care contracts: a healthcare administrator's playbook

You run an independent practice. Margin has compressed three years running, you carry 20 to 30 insurer deals, and if you are honest, you do not know which managed care contract is your worst performer. A managed care contract is an agreement between a healthcare provider and a health insurance company that defines covered services, including reimbursement rates, and the terms and conditions under which you deliver patient care. Put more formally, a managed care contract is a legal agreement between a provider and a managed care organization (MCO), and every operations lead signs dozens of them without ever ranking one against another.

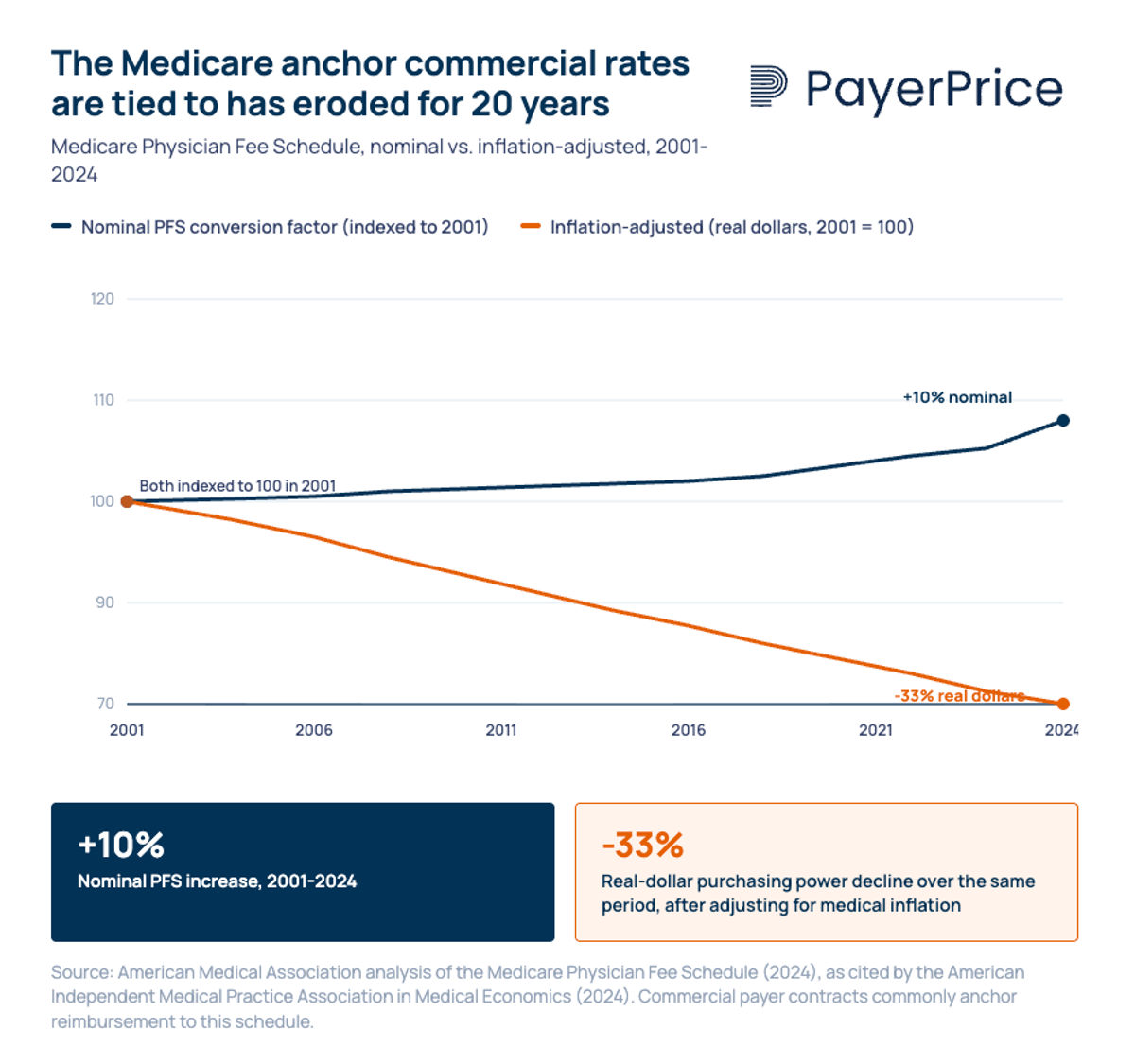

According to the American Independent Medical Practice Association, payments to clinicians under the CMS fee schedule rose 10% in nominal terms over 20 years, which translates to a roughly 30% real-dollar decrease after inflation. Commercial insurers anchor reimbursement to that eroded rate. Hospital systems negotiate up from it. Independent medical groups, more often than not, accept what is on the page.

"You could be 15 percent behind market if you don't know where market sits from a data standpoint."

- Mark Schroeder, VP Growth at Aroris Healthcare and former UnitedHealthcare network executive, DocBuddy Journal podcast

This article is the playbook most writing on the topic skips: rate benchmarking, clause-level counter-language, a 12-month calendar, and the leverage medical groups actually have. Every section pairs a common pain with a specific tactic. You will finish with a repeatable approach that does not rely on another consulting deck.

Why medical groups lose managed care contract negotiation before it starts

Most medical groups lose rate before they sit down to discuss a managed care contract because they have no comparative view of their existing contracts. A single operations lead carries 20 to 30 insurer arrangements, each with its own fee table, amendment history, and renewal timeline. Without a comparative view, there is no way to rank what is underperforming and no way to navigate a rate review with credibility.

Doral Jacobsen, FACMPE, CEO of Prosper Beyond, describes the pattern in Physicians Practice:

"So many practices don't really know how their contracts are performing. They're not sure what their reimbursement rates are."

- Doral Jacobsen, FACMPE, CEO, Prosper Beyond

Jacobsen describes a Florida client with eight Medicare Advantage health plans. The group had already picked which agreement it wanted to renegotiate first. Once she ran a comparative view, that deal was not even the worst one. They were arguing about the wrong contract.

The bandwidth math explains the rest. According to Schroeder, a single rate conversation with a large insurer averages 80 to 100 touchpoints. Multiply that by a stack of 25 agreements and a one-person back office, and proactive renegotiation stops happening. Groups default to signing what arrives, and administrative burdens on the provider side grow every year.

Solve the information problem and most of the leverage problem disappears. That starts with knowing which plan designs you are contracting against.

Types of managed care plans: how each care plan shapes your contract

The purpose of managed care is to control healthcare costs by tying reimbursement to a defined network, a defined utilization review process, and a defined care plan structure. Four plan designs dominate commercial healthcare services, and each shapes how a deal reads.

- HMO (health maintenance organization). HMO plans require patients to stay within the network for routine medical services, and a primary care clinician coordinates referrals. These designs usually include tighter utilization management and capitation options.

- PPO (preferred provider organization). PPO plans offer flexibility to see out-of-network clinicians at higher cost, written fee-for-service with network-based discounts.

- POS (point of service). This design combines gatekeeping with out-of-network flexibility. Patients can go outside the network, but costs outside the network rise sharply.

- EPO and narrow-network variants. Strict in-network-only designs that behave like a tightened HMO without the primary care gatekeeper.

Every care plan above sits inside an insurance plan written by one of a handful of large insurers or a regional MCO. Those plans are what you are actually contracting against inside the broader healthcare system. A group that signs one deal to cover every product line without differentiating designs is almost always mispricing at least one of them.

Key components of a managed care contract for healthcare providers

Every managed care contract shares the same key components, and the clinical and financial risk sits in how those components interact, not in the definitions themselves. Carefully review each one before you sign.

The components of a managed care contract for any provider are:

- Covered services and exclusions. Define what medical care is in scope, which CPT codes are included, which require prior authorization, and which are explicitly excluded.

- Reimbursement. The table of services at negotiated rates, usually expressed as a percent of the federal anchor or a flat fee per CPT.

- Credentialing and network participation. Terms and conditions for joining the network, continuing participation, and re-credentialing cycles.

- Utilization management and medical necessity. How the MCO reviews claims, how clinicians submit claims, and how write-offs are appealed.

- Claims submission and payment terms. Timely-filing windows, clean-claim definitions, and insurer payment obligations.

- Term, renewal, and termination. How long the deal runs, whether it auto-renews, and what notice is required to terminate.

- Amendment and compliance language. Who can change the contract terms, under what notice, and which regulatory requirements apply.

- Quality of care and performance metrics. HEDIS, Star Ratings, and any value-based adjustments that modify baseline pay.

A deal that does not clearly outline each of these key components will cost the healthcare provider money later. Carefully review the exact language, not just the summary.

Benchmarking: how to negotiate fair healthcare rates

Fair means your commercial rates sit at or above the metro median for your specialty, expressed as a percent of the federal fee table for each CPT you actually bill. Without that number, "fair" is whatever the insurer said last.

Four data sources give a medical group a defensible benchmark in 2026:

- Federal fee table. The universal anchor. Express every commercial rate as a percent of the federal rate by CPT.

- Transparency in Coverage machine-readable files. Under the federal Transparency in Coverage rule, every insurer discloses the rate it pays each of its network providers for each code.

- PayerPrice. Peer benchmarks by specialty, region, and group size.

Rank your portfolio once the numbers are in. Score each managed care contract on three axes: rate position (percent of the federal anchor against metro median), volume (annual billed charges), and growth outlook (is the insurer expanding or shrinking). The lowest scores are the ones to renegotiate first; the highest scores are the ones to protect.

A rate-review request without this math is a wish list. A rate-review request with it is a negotiation, and it is how providers maximize pay without waiting for the insurer to act first.

Red-flag clauses to negotiate back in any managed care contract

The clauses that cost the most money sit on the standard insurer template and get signed because no one reads them against a counter-proposal. Each one below has cost medical groups meaningful revenue. Each comes with what to send back.

- All-products clauses. Force the group to accept every product line at the same rate. Counter: require product-by-product opt-in with separate rate tables, explicitly naming each health insurance product in and out.

- Unilateral amendment on 30 days' notice. The insurer reserves the right to change the rate sheet or policy. Counter: require mutual written consent for any material change to the managed care contract, define "material" in the contract terms, and preserve termination without penalty if it is invoked.

- Evergreen auto-renewal with a 90-day notice-to-terminate. Creates a renewal cliff most groups miss. Counter: replace with a hard expiration date that requires affirmative written renewal.

- Timely-filing windows shorter than 180 days. Counter: 180-day minimum, paired with insurer-side 30-day clean-claim payment.

- Recoupment and retroactive-denial lookback windows. Counter: cap at 12 months or the state statutory maximum, whichever is shorter. Prohibit offset against unrelated claims.

- Silent PPO and rental-network clauses. Your rates end up on networks you never contracted with. Counter: explicit opt-in per downstream network, listed as an exhibit.

- Medical-necessity sole-discretion language. This ties directly to appeal mechanics.

"Some stories have outlined Cigna medical directors denying things once every 1.2 seconds. Well, I have met some really gifted clinicians, and none of them can do a diagnosis in 1.2 seconds."

- Ron Howrigon, President and CEO, Fulcrum Strategies, SoundPractice podcast

Counter: require medical-necessity decisions to reference published evidence-based criteria (MCG, InterQual) and require same-specialty review on appeals.

- Downcoding authority. Counter: prohibit code changes without a documented medical-record review and a written EOB identifying the reviewing clinician.

Practice manager Lynne Leis caught a Cigna deal paying below the federal benchmark because she ran the math.

"Cigna didn't even know that its rates were below Medicare. But I was the only one who called."

- Lynne Leis, practice administrator, Physicians Practice

Pushing back in writing, on specific clauses, with proposed counter-language, signals to the insurer that you are a group that reads closely. Insurers price contracts differently against groups that read.

Best practices for managed care contract management

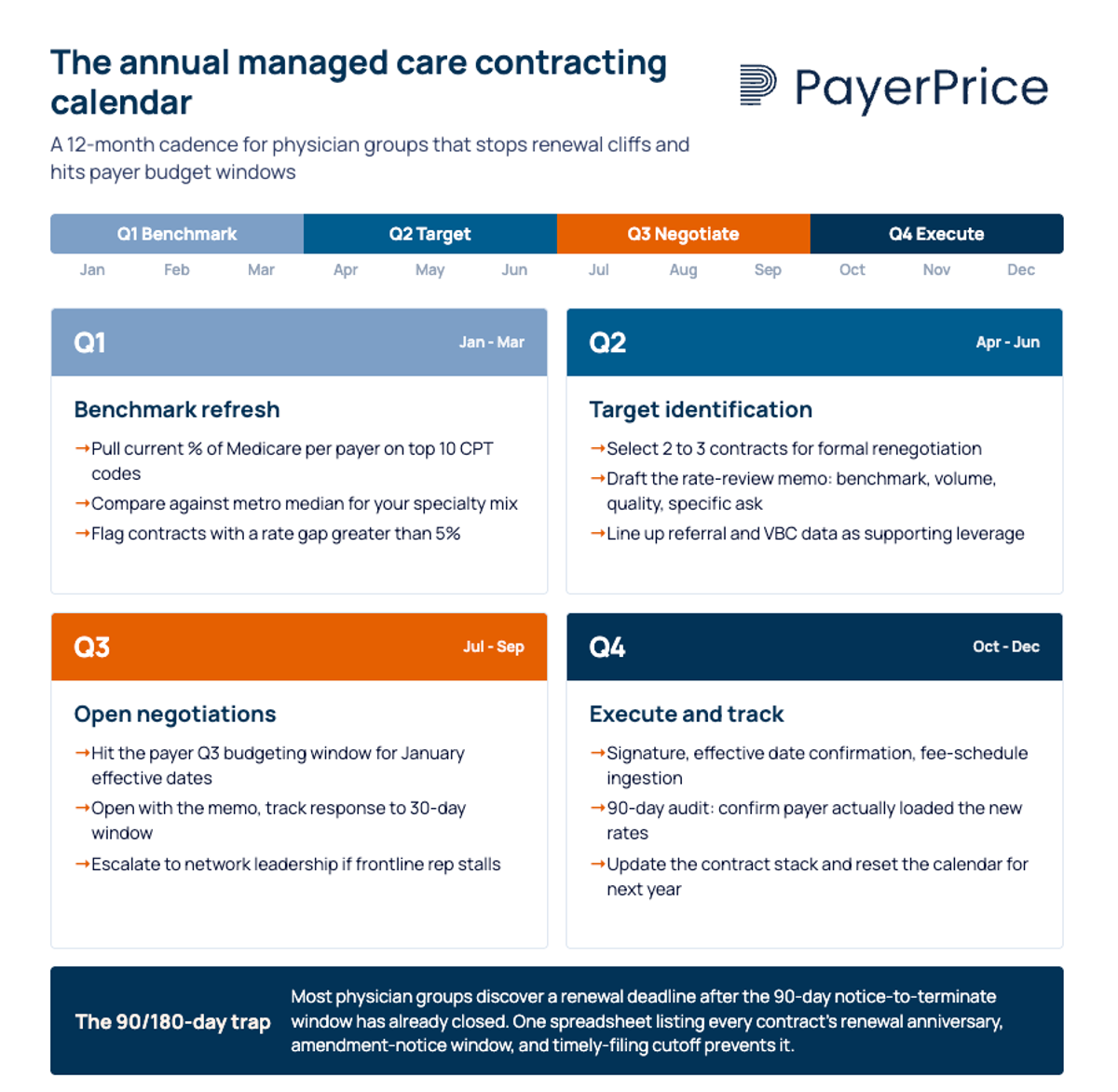

A simple annual cadence stops renewal cliffs, streamlines review, and hits insurer budget windows. The specific timeline looks like this:

- Q1, benchmark refresh. Pull current rates per insurer and compare against metro median. Flag any deal where the gap exceeds 5%.

- Q2, target identification. Select two to three managed care contracts for formal renegotiation. Draft the rate-review memo with benchmark, volume, quality scores, and a specific ask.

- Q3, open negotiations. Most commercial insurers budget rate changes in Q3 for January effective dates.

- Q4, execute and track. Signature, effective date confirmation, rate-sheet ingestion, and a 90-day audit to ensure the insurer loaded the new rates.

The 90/180-day trap is the single biggest calendar failure. Most groups discover a renewal deadline after the 90-day notice window has already closed. A one-page artifact listing every deal's renewal anniversary, amendment-notice window, and timely-filing cutoff prevents it and helps you optimize every other tactic in this article, keeping groups of hospitals and independent practices alike from slipping into another stale year.

The same cadence applies to managing leverage against insurers. Medical groups underestimate what they actually carry:

- Geographic patient share. If you represent more than 15% of an insurer's in-network volume for a specialty in a metro, the insurer has a network-adequacy problem the moment you signal exit.

- Quality scores and Star-rating contribution. MA plans are paid partly on HEDIS and Star Ratings. High-quality performance is leverage that does not appear on a fee table.

- Referral network influence. Primary care groups driving referrals to preferred specialists carry embedded leverage even when unit rates look modest.

- Willingness to take risk. A group open to shared-savings or capitation arrangements carries more weight than one insisting on pure fee-for-service.

- The credible walkaway. Most groups never signal it, so insurers assume they never will.

Dr. David Eagle of New York Cancer & Blood Specialists frames the stakes:

"At some point maintaining an independent practice the numbers don't pencil out when the costs go up, but the reimbursement doesn't. Hospitals can often negotiate higher commercial rates with the private insurers."

- Dr. David Eagle, MD, Partner, New York Cancer & Blood Specialists

Package the leverage into a three-page rate-review memo: benchmark gap first, then volume, quality impact, referrals, and a specific ask with a 30-day response window. A memo that reads like a negotiation document gets handled differently than an email asking for more money.

When contracts fail: management software and accounts receivable protection

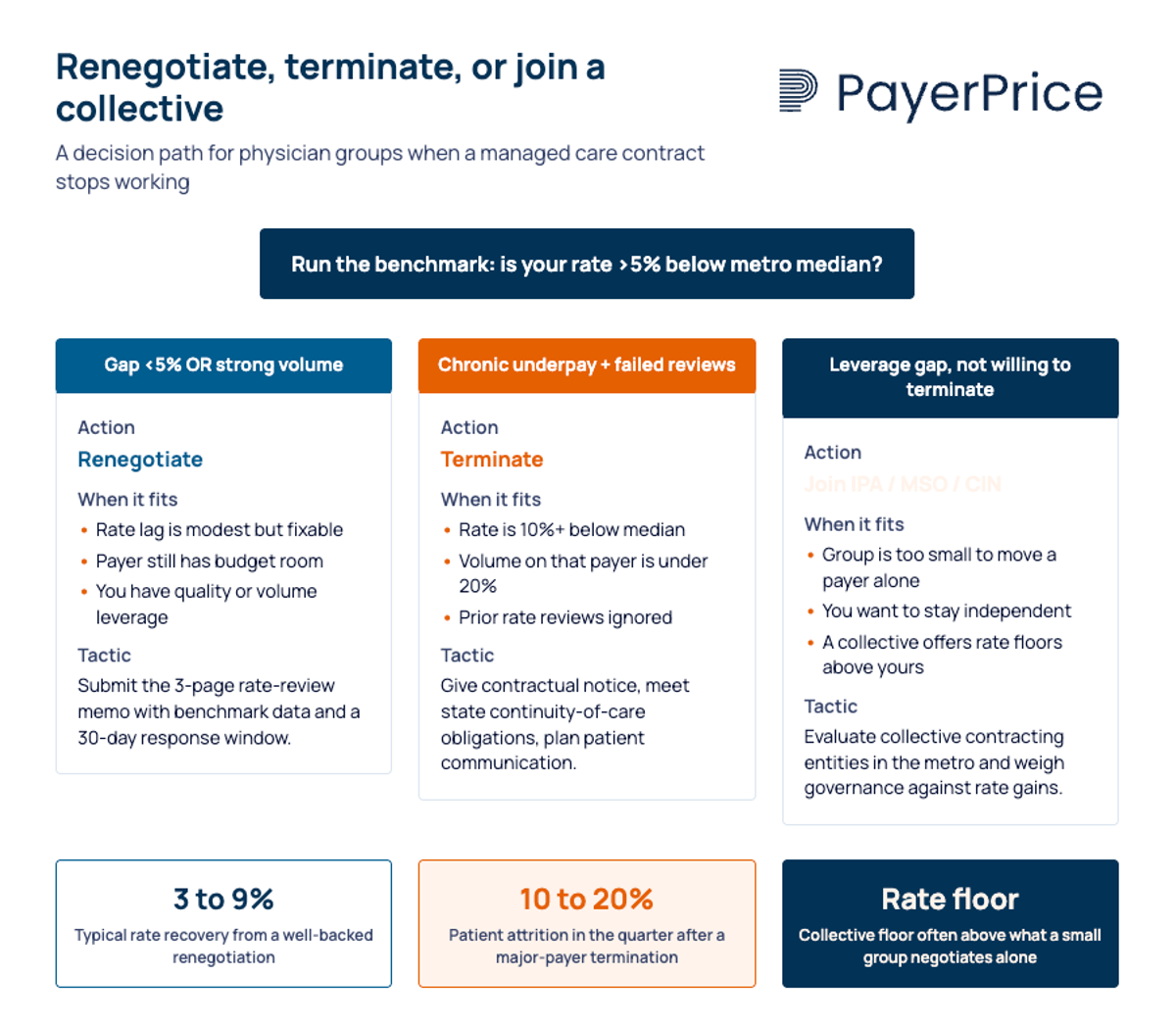

When renegotiation fails, a contract repository tool and tight cash-collection controls keep the rest of the care industry economics from absorbing the damage. Ending a deal is a last-resort tool, but it has to be on the table for leverage to be real.

End the contract when the data supports it: chronic underpayment that benchmark data confirms and the insurer refuses to address; a pattern of unilateral amendments that erode rate faster than you can recover; or write-off rates so far outside peer norms that the contracted level of care economics become a fiction. Provide contractual notice, follow state continuity-of-care requirements, and communicate the change to affected patients in writing.

The non-nuclear alternative is collective contracting. Dr. Paul Carlan, president and CEO of Valley Medical Group, joined an IPA rather than be acquired by a hospital system. An Independent Practice Association concentrates contracting into a function staffed for it and gives participants access to rate floors individual groups cannot command.

Two operational tools protect cash flow no matter which path you choose:

- Contract management software. A lightweight tool that tracks contract terms, renewal dates, amendment notices, fee tables, and insurer obligations. Streamline the back office by centralizing every document, and you stop losing deals in shared drives.

- Receivables discipline. Track write-off trends by insurer and CPT. Escalate any plan whose behavior moves outside a reasonable band, and tie that data back into the next benchmark refresh. Silent reductions are the second rate cut nobody sees.

Run the math before pulling any trigger. A deal that pays 15% below the metro median on your top-five CPT codes across 20% of your volume usually justifies an exit. A lag that pays 5% below median across 5% of your volume usually does not. Benchmarking tells you which situation you are in and ensures you do not end a relationship you could have saved.

Start with the data, this quarter

Understanding managed care is not about memorizing definitions. It is about knowing which of your existing contracts is underperforming, by how much, and against what benchmark. The groups that hold rate in 2026 rank every deal against the federal anchor, keep a clause playbook, run a 12-month cadence, and package their leverage in writing.

If you do not have a comparative view across your contracts today, build one this quarter. Rank your insurers on rate position, volume, and growth outlook. Flag the worst performer. Draft the rate-review memo. Delivering quality patient care depends on keeping the back-office economics sound, and the back-office economics depend on reading every deal as if it costs you money, because it does.

Share this article

Help spread the knowledge by sharing with others

Ready to see how your rates compare?

PayerPrice gives you instant access to negotiated rate data across payers and providers so you can benchmark, negotiate, and optimize with confidence.

Related Articles

Continue exploring healthcare transparency and compliance topics

Value-Based Contract Guide for Physician Groups & Value-Based Care

Navigate value-based care contracts with our guide for physician groups. Learn about risk-sharing agreements, payer incentives, and real-world quality metrics.

How to Model a Payer Contract: A Provider's Guide

See how providers model payer contracts against real claims to catch a money-losing deal before signing. Formulas, a worked example, and a 5-step method.

How to Run Payer Contract Analytics (Physician Group Guide)

Stop signing stealth pay cuts. This guide shows physician groups how to benchmark rates, recover underpayments, and run payer contract analytics in-house.