How to Contract With Insurance Companies (Without a Bad Rate)

How to contract with insurance companies as a provider: the credentialing steps, the contract clauses to check, and how to tell if your rate is fair before you sign.

Cameron Fletcher

Head of Growth at PayerPrice

You can be the best clinician in your zip code and still not get paid for the work. Before an insurance company sends a single dollar to your practice, you have to contract with it: get credentialed, get accepted in-network, and sign a fee schedule. Most providers treat that fee schedule as a formality to rush through so they can start seeing patients. It is the most expensive decision in the entire process.

The number you sign compounds. It applies to every claim you submit for years, and many payer contracts forbid you from renegotiating for three years after you sign. The rate also tends to erode while you wait. One solo physician documented how his contracted rate, set at 80% of Medicare when he opened, slipped to 71.9% of Medicare over a few years as Medicare itself failed to keep pace with inflation. Worse, most contracts include a clause that bars you from discussing your rate with anyone, so you sign blind and find out later whether you got a fair deal.

How unfair can it get? According to KFF's review of the research, private insurers pay physicians 143% of Medicare rates on average, but that figure ranges from 118% to 179% across studies. Two practices billing the same code to the same payer in the same market get paid wildly different amounts. And the contract you just signed tells you that you are not allowed to compare notes.

This guide walks you through the full path to contract with insurance companies, from credentialing to a signed contract, and it does the thing the rest of the internet skips: it shows you how to tell whether the rate you are offered is fair before you lock it in.

Credentialing vs. contracting: what "contracting with insurance companies" actually means

Contracting with an insurance company means agreeing to its fee schedule and network terms, while credentialing means the insurer verifying your qualifications. They are two separate steps, and being credentialed does not mean you have a signed rate. Providers conflate the two constantly, which is how people end up surprised that "approved" did not mean "paid well."

Credentialing is the background check. The payer confirms your license, education, training, malpractice history, and work history. Contracting is the business agreement that follows: the document that states what the insurer pays you for each service, how fast it pays, and what rules you agree to follow. You complete credentialing once to prove you are qualified. You live with the contract every day you practice.

Part of why this trips up new practice owners is that nobody teaches the language. Amy Plano, a registered dietitian who now coaches other clinicians through the process, put it bluntly:

"Raise your hand if your dietetics program taught you the Krebs cycle but not how to submit an NPI application. Credentialing requires learning a whole new language, EFTs, CAQH, taxonomy codes, and figuring it out on your own can take years."

- Amy Plano, RD, The Reimbursement Dietitian

The terms you need to recognize are few. Your National Provider Identifier (NPI) is your unique ID number. Your CAQH profile is the central database payers pull your credentials from. The fee schedule is the list of dollar amounts the payer pays per billing code. The allowed amount is what the payer actually approves on a given claim. And the most important benchmark in the whole system is the percentage of Medicare your commercial rate represents, because nearly every payer sets its rates as a multiple of what Medicare pays. Get comfortable with those five terms and the rest of the process stops feeling foreign. The first real decision is which payers to pursue.

Which insurance companies should you contract with first?

Contract first with the payers that cover the largest share of your local patients and reimburse your highest-volume billing codes. Applying to every insurance company at once wastes months and buries you in paperwork for plans that send you two patients a year.

Start with your own numbers. Identify the handful of billing codes that generate roughly 75% of your revenue, then figure out which insurers dominate your area and your specialty. A pediatric therapist in one metro and a cash-heavy dermatologist in another have completely different priority lists. Rank the payers by how many of your prospective patients carry their cards, and apply to those first.

Before you sink time into an application, confirm the panel is open. Insurers close networks when they decide an area has enough providers of your type, and they reject applicants on "network adequacy" grounds no matter how qualified you are. Andy Turner, a naturopathic doctor running a solo practice in Oregon, ran straight into this:

"Despite the ongoing shortage of primary care providers, some insurance networks are currently closed to new clinicians. PacificSource is currently closed to new provider applications. Moda has not returned phone calls or emails."

- Andy Turner, ND, AndyND

If a panel is closed, you have three moves: ask to be added to the waitlist, file a network-adequacy appeal arguing that local patients lack access to your specialty, or focus your energy on the open panels that cover the same patients. Chasing a closed panel with repeated identical applications gets you nowhere. Once you have a prioritized, confirmed-open list, the paperwork begins.

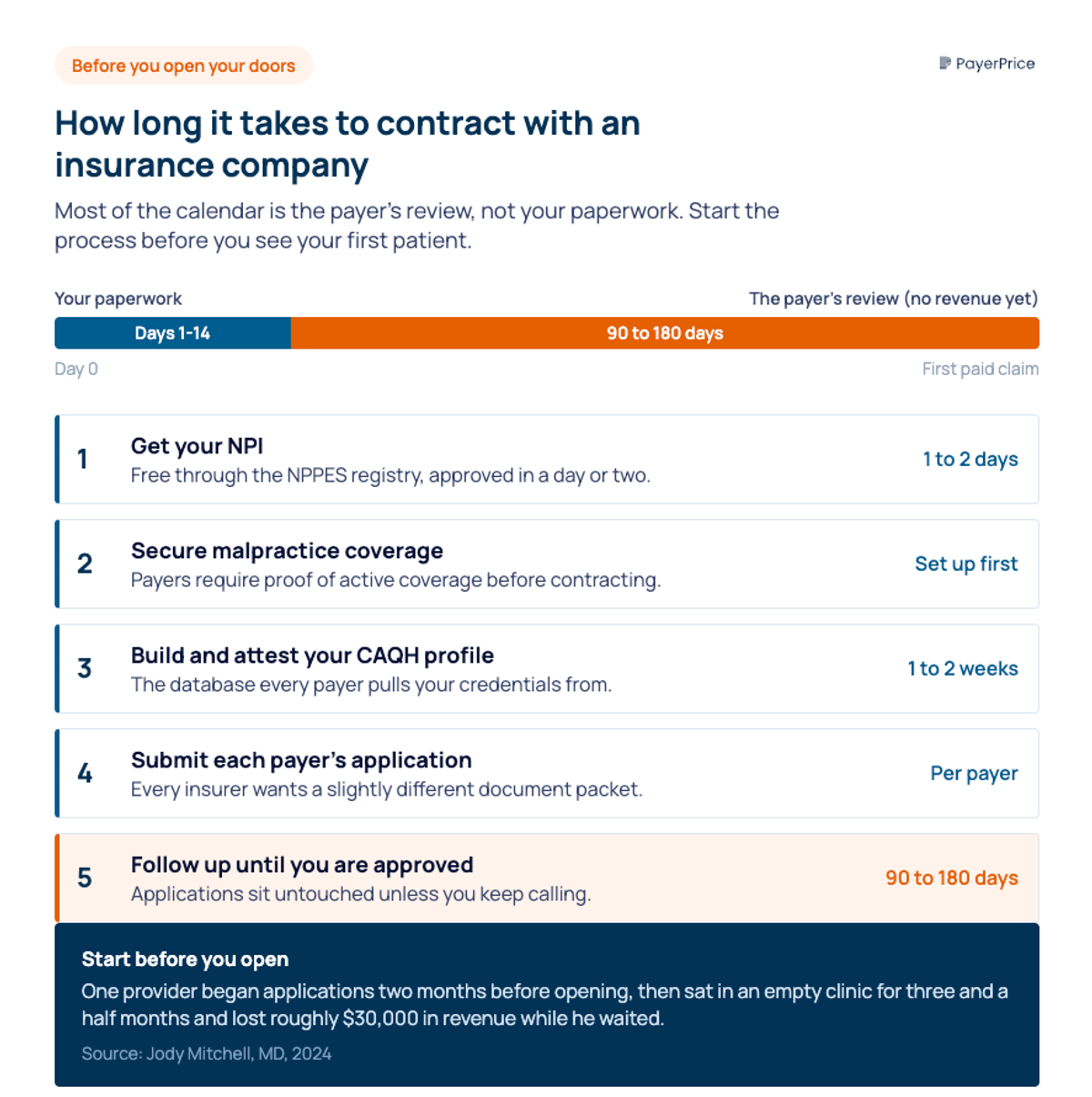

How to contract with insurance companies, step by step

The process runs in a fixed sequence: get your NPI, secure malpractice coverage, build your CAQH profile, submit each payer's application, and follow up until you have a signed contract. Five steps, and the order matters because each one feeds the next.

- Get your National Provider Identifier. Apply through the NPPES registry. It is free, and most applications come through in a day or two. Solo providers need a Type 1 (individual) NPI; if you bill under a practice entity, you also need a Type 2 (organizational) NPI.

- Secure malpractice insurance. Payers require proof of active coverage before they contract with you, so line this up early.

- Build and attest your CAQH profile. This is the database payers pull from, and an incomplete or unattested profile stalls every application behind it.

- Submit each payer's application. Every insurer wants a slightly different packet, which is the single most maddening part of the job. As Amy Plano describes it, "Blue Cross might ask for one set of documents, Cigna another, and Medicare a different set."

- Follow up relentlessly. Applications sit untouched unless you call. Track every submission, every contact name, and every promised date.

Plan on 90 to 180 days from submission to a usable contract, and start before you open your doors. The cost of starting late is concrete. In one account documented by Jody Mitchell, MD, a provider who began his applications just two months before opening sat in an empty clinic for three and a half months and lost roughly $30,000 in revenue while he waited for approvals.

Sherri Webster, an LCSW who switched to private pay partly because of this grind, described the waiting plainly:

"It means submitting the same documents to multiple panels, waiting anywhere from 90 to 180 days for approval, following up repeatedly with people who may or may not call back, and sometimes, after months of paperwork, being told the panel is closed. No clients. No reimbursement. Just time."

- Sherri Webster, LCSW, Rising Sails Counseling

Getting credentialed and accepted is the part everyone focuses on. The contract that lands in your inbox afterward is where your income is actually decided.

How to read the contract before you sign

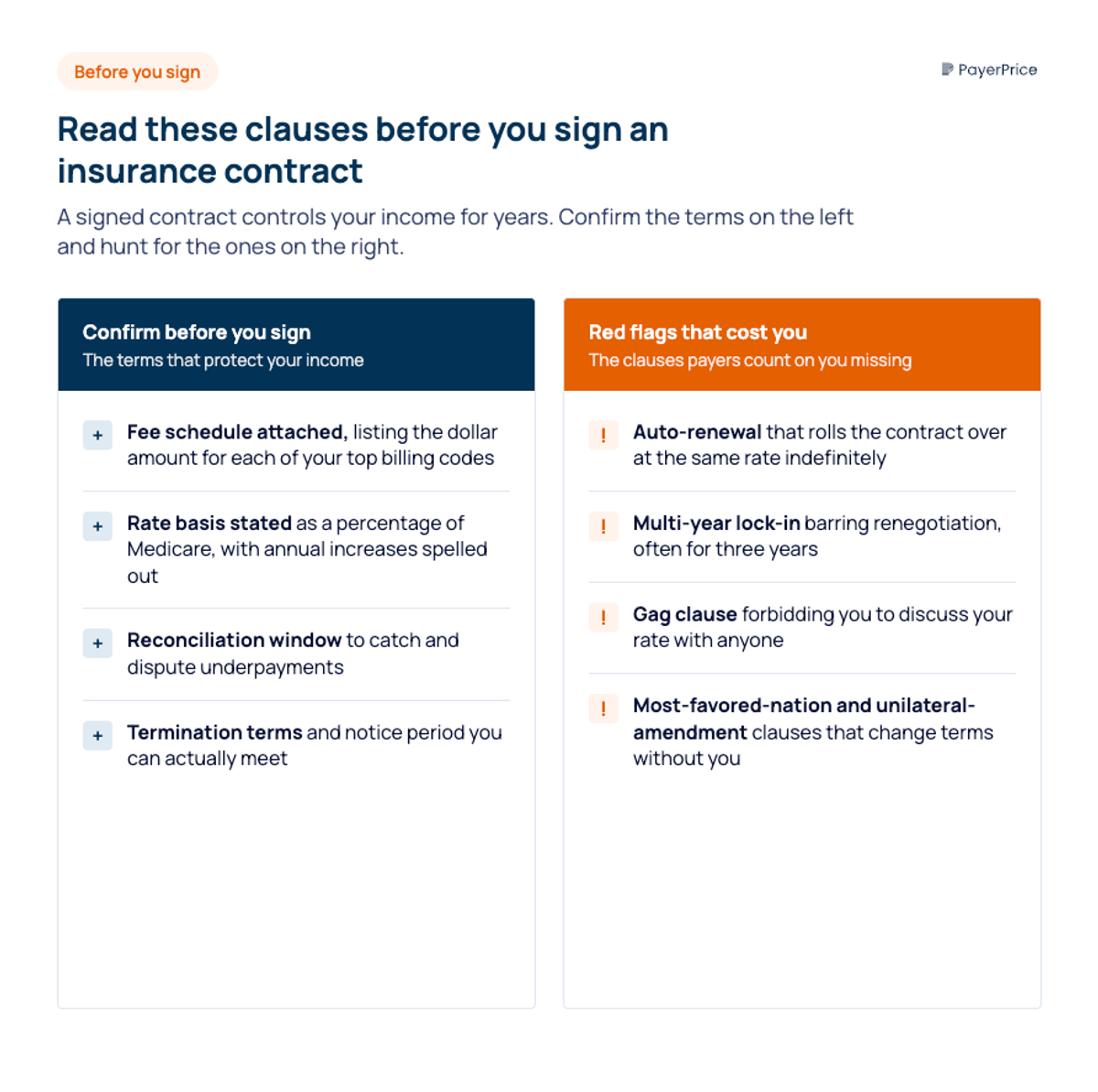

Never sign a payer contract without an attached fee schedule, and read every clause that controls how and when you get paid. A contract without a fee schedule is a contract to be paid an unknown amount, and signing one hands the payer total control over your income.

Once the fee schedule is attached, work through the clauses that determine what the contract actually costs you. Check each of these before you sign:

- The fee schedule itself, listing the dollar amount for each of your top billing codes, not a vague reference to a schedule "available upon request."

- The rate basis, which states whether your rates are a percentage of Medicare, a fixed fee schedule, or something else, and whether they increase each year.

- The auto-renewal, or "evergreen," term that rolls your contract over at the same rate indefinitely unless you act.

- The lock-in period, which dictates how long you wait before you can renegotiate. Many run three years.

- The gag clause that forbids you from discussing your contracted rate with billers, colleagues, or anyone else.

- The timely-filing limit, which is the deadline to submit a claim before the payer refuses to pay it.

- The reconciliation window, which is how long you have to catch and dispute an underpayment.

- Most-favored-nation and unilateral-amendment clauses, which let the payer change terms or demand your lowest rate without renegotiating.

These clauses are not theoretical.

Dr. Maria Ingalla, a psychiatric nurse practitioner, discovered the cost of the gag clause and the reconciliation window the hard way after a payer processing error wrote her in at a rate 10% below every peer in her specialty:

"There's a clause in the contract that you are not allowed to discuss your contracted rate with your biller, your business associates, no one. So you sign that contract blindly as a new contractor with a practice, and then we all get to wait and see if the payments are equal."

- Dr. Maria Ingalla, PMHNP, Paperflower Psychiatry

She did not catch the error until the business was visibly losing money, well past the window to fix it cleanly. Reading the clauses protects you from that fate. But the clauses are only half the contract. The number on the fee schedule is the other half, and knowing whether that number is any good is a separate skill.

How to know if your reimbursement rate is fair, and negotiate it

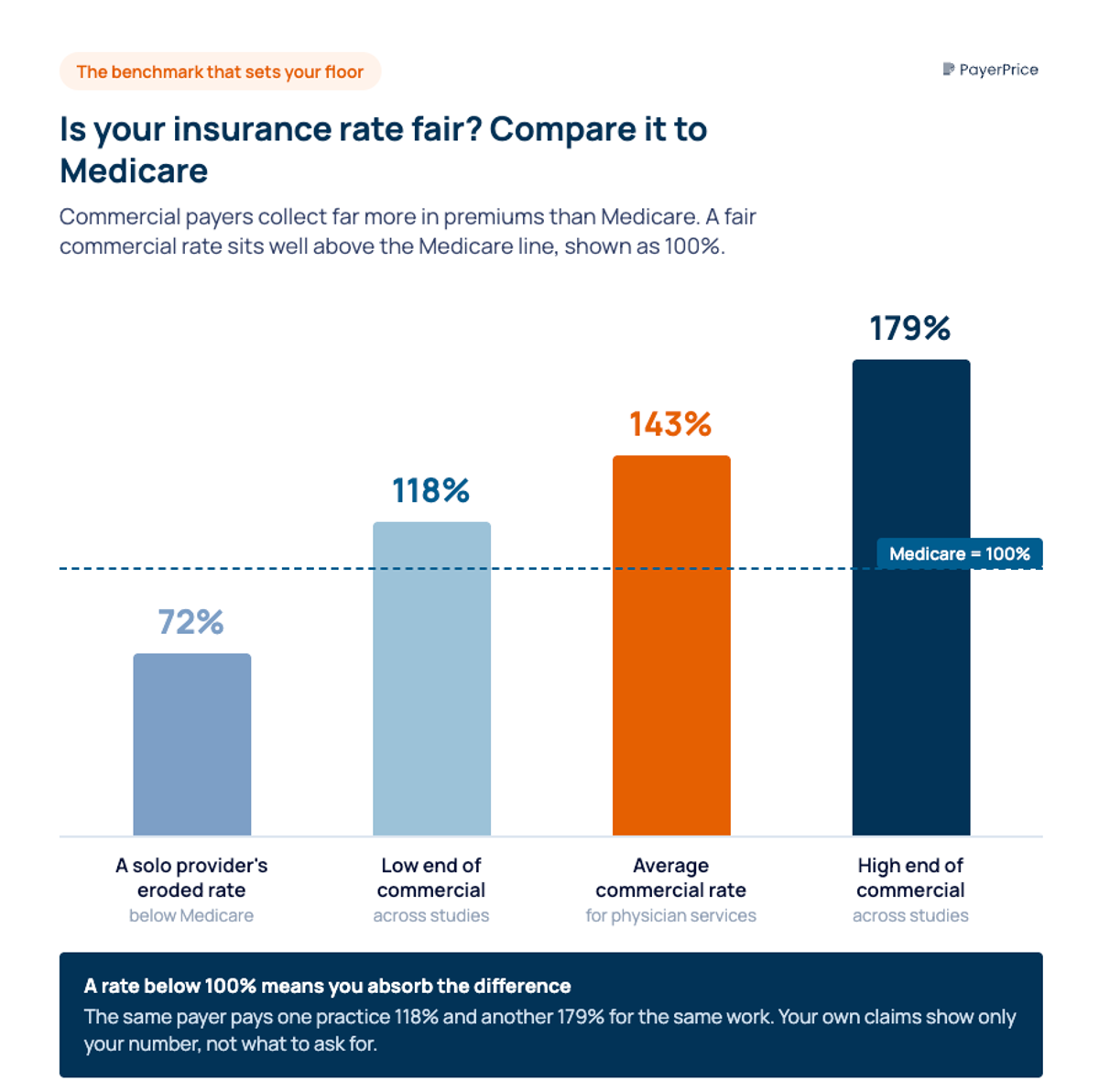

A fair commercial rate sits well above Medicare, not below it, so compare every offered rate against the current Medicare rate for your highest-volume codes. Commercial insurers collect far more in premiums than Medicare pays out, and a rate that matches or undercuts Medicare means you are absorbing the difference.

The math sets your floor. According to KFF's review of the literature, private insurers pay physicians 143% of Medicare on average. Pull the current Medicare rate for each of your top codes, divide the payer's offered amount by it, and you have an instant read on where the offer falls. An offer at 90% of Medicare is below the floor. An offer at 110% is below average. The starting method is a simple spreadsheet: list your highest-volume codes, the annual volume of each, the current Medicare rate, and the payer's offered amount.

Here is the limit of that method, and the gap nobody fills. Medicare and your own claims history only tell you what you make. They tell you nothing about what the practice across town earns from the same payer for the same code. The KFF range of 118% to 179% means the spread between a weak rate and a strong one is enormous, yet the gag clause in your contract forbids you from asking your peers, and provider associations are barred by antitrust law from sharing rate data. That information gap is the single biggest reason solo providers accept low rates: they have no way to know a low rate when they see one. External market reimbursement benchmarks close that gap by showing you what a specific payer actually pays other comparable providers in your market, which is the leverage the existing guides admit you need and never supply.

Armed with a real benchmark, you negotiate from facts instead of hope. Ask for a rate above Medicare and justify it with your data. Do not accept "the panel is full" as the end of the conversation, and do not accept the first low number, because the rate you sign becomes the baseline every future payer negotiates against. Brad, the physician who watched his rate erode, learned how hard payers push:

"My lowest payer told me that if I do not like the rate they proposed, they are happy to withdraw the offer since they do not need me in my area. I recall the network representative telling me exactly how many other doctors in my specialty were in my surrounding area."

- Brad, MD, InvestingDoc

That pressure works on providers who have nothing to counter with. It works far less on a provider who can point to the market rate and show that the offer sits at the bottom of it.

Ready to see how your rates compare?

PayerPrice gives you instant access to negotiated rate data across payers and providers so you can benchmark, negotiate, and optimize with confidence.

Get in-network on terms you chose

Contracting with insurance companies is not hard to do. Getting contracted at a rate you actually chose on purpose is the part that takes work, and it is the only part that determines whether your practice makes money. The administrative steps get you in the door. The fee schedule decides what happens after.

Your first move today is concrete: list the ten billing codes that drive most of your revenue, look up the current Medicare rate for each, and calculate where any contract you already hold or any offer in your inbox falls as a percentage of Medicare. If a number comes in below 100%, you have found a renegotiation target. If you do not yet know what other practices earn from that same payer, that is the gap to close before you sign anything, because once you sign, the rate is yours for years.

Share this article

Help spread the knowledge by sharing with others

Ready to see how your rates compare?

PayerPrice gives you instant access to negotiated rate data across payers and providers so you can benchmark, negotiate, and optimize with confidence.

Related Articles

Continue exploring healthcare transparency and compliance topics

How to Model a Payer Contract: A Provider's Guide

See how providers model payer contracts against real claims to catch a money-losing deal before signing. Formulas, a worked example, and a 5-step method.

How to Run Payer Contract Analytics (Physician Group Guide)

Stop signing stealth pay cuts. This guide shows physician groups how to benchmark rates, recover underpayments, and run payer contract analytics in-house.

Multi-Specialty Coding Guide: Billing in Multi-Specialty Practices

A multi-specialty coding and billing guide for physician groups. Covers CPT, modifier 25, NPP rules, and fee schedules in multi-specialty practices.