5 Payer Contract Red Flags to Look For

The contract you signed looks fair on paper. But buried in the fine print are clauses that let payers rewrite your rates, claw back payments from years ago, and downcode your claims without reviewing a single chart. Here are the five red flags that cost providers the most money, and how to spot them.

Cameron Fletcher

Head of Growth at PayerPrice

Your payer contract says you'll be reimbursed at 110% of Medicare. On paper, that looks fair. Then the denials start. Claims get downcoded. A recoupment letter arrives for services you provided two years ago. By the end of the quarter, your actual reimbursement is closer to 85% of Medicare, and nothing in your billing system flagged the difference.

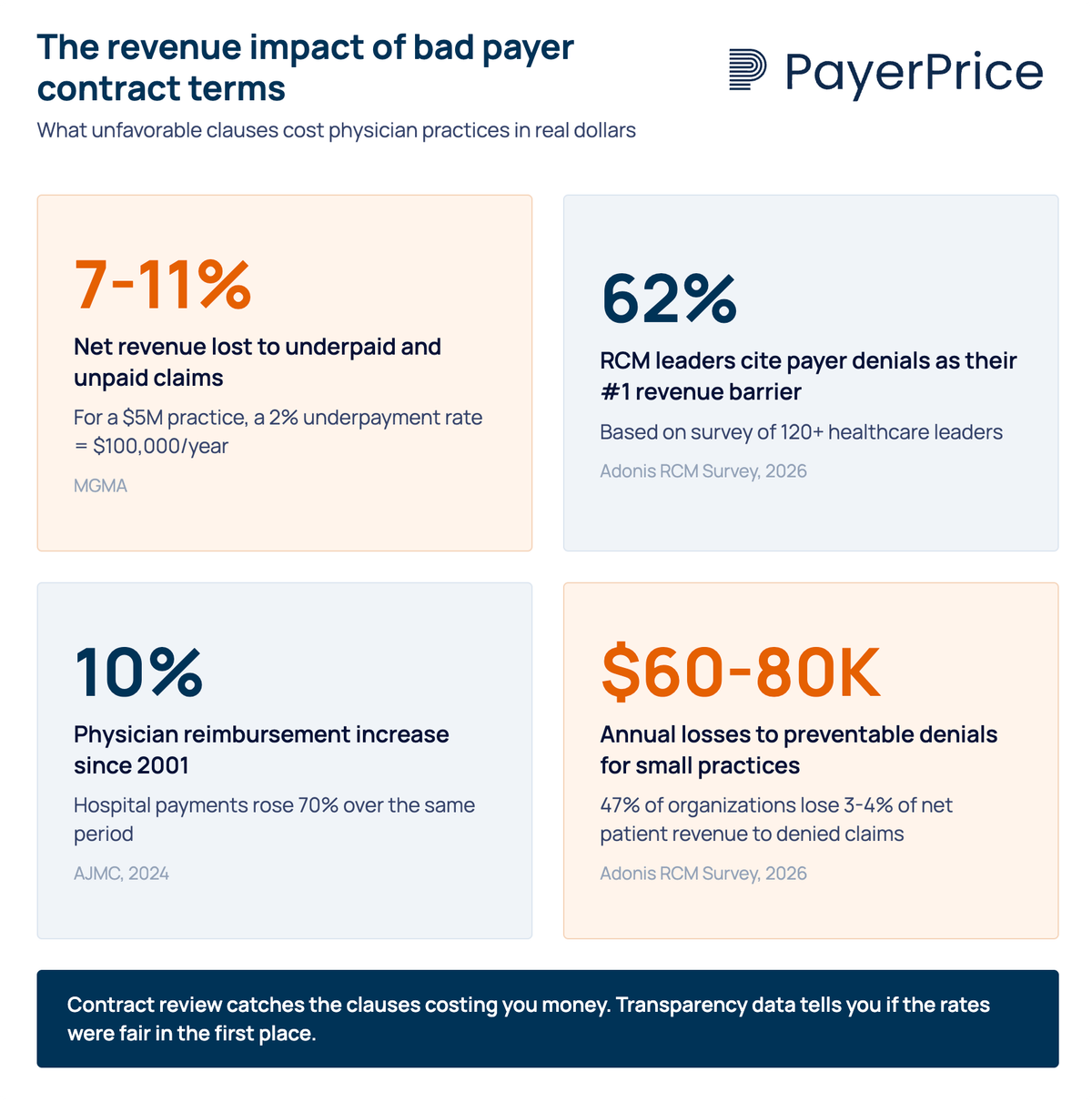

This is not a hypothetical. According to MGMA, physician groups lose between 7-11% of net revenue to underpaid and unpaid claims. For a $5 million practice, even a 2% underpayment rate adds up to $100,000 per year. And that figure only counts claims where the payer pays less than the contracted rate. It does not account for contracts that were poorly structured in the first place.

"It's a tragic story that's all too common: a hardworking physician practice owner, busy with a full schedule of patients, is thrilled with the new contract she negotiated from a major Medicare Advantage payor. On paper, the payor agrees to reimburse the practice well. Then reality hits. The denials start piling up."

Scott Dewey, Chief Managed Care Officer at PayrHealth

The gap between what a contract promises and what it actually pays comes down to specific clauses buried in the agreement. These are the five payer contract red flags that cost providers the most money, along with the contract language to look for and the data you need to push back.

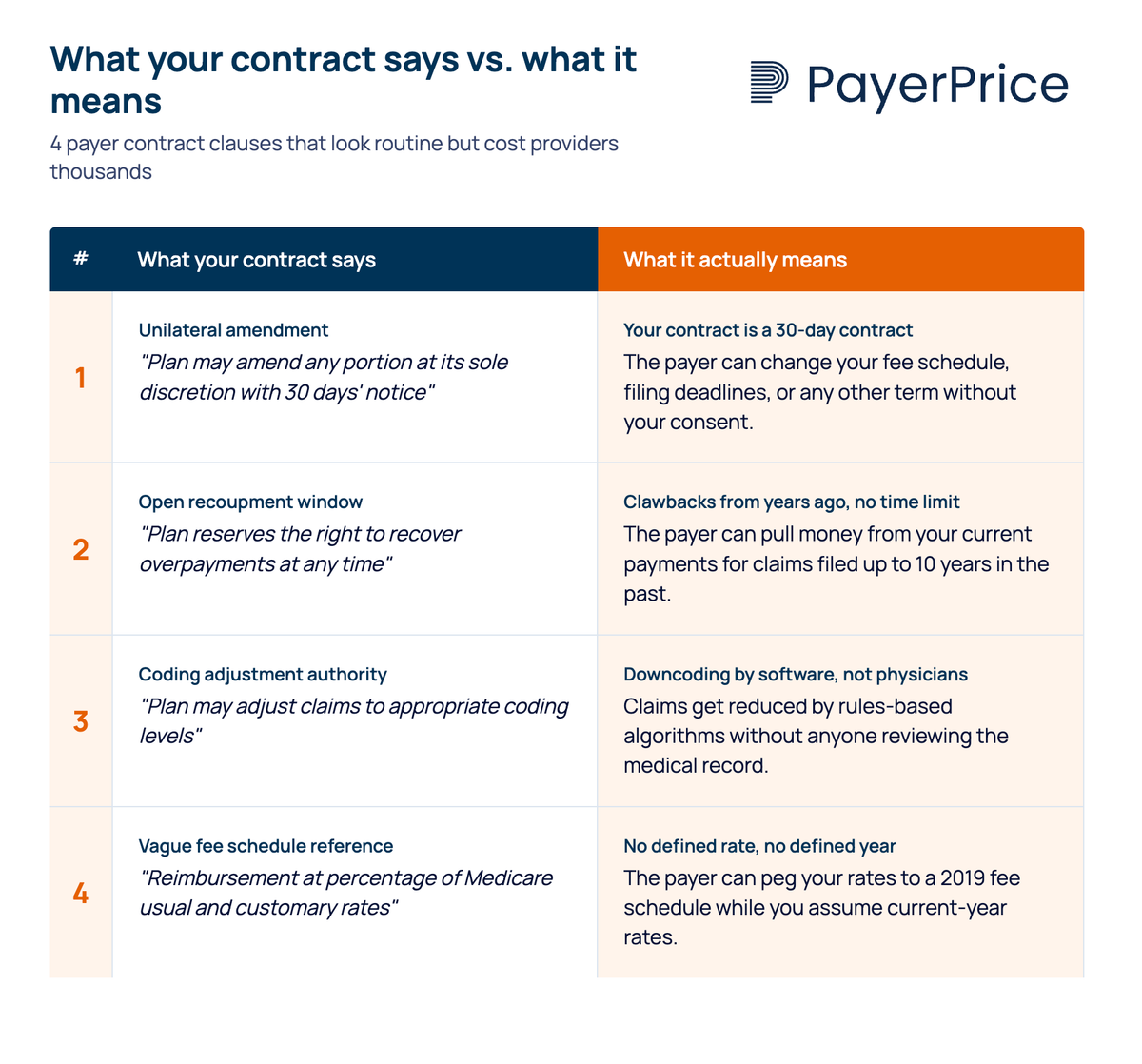

1. Unilateral amendment clauses let payers rewrite your contract after you sign it

A unilateral amendment clause gives the payer the right to change any term in your contract, including your fee schedule, with minimal notice and no requirement for your consent. The typical version requires only 30 days' written notice, sometimes delivered by posting an update on the payer's website.

A common version reads something like: "Health plan may amend any portion of the contract at its sole discretion by giving the provider 30 days' notice." In practice, this turns a multi-year agreement into a 30-day contract. The rate you negotiated today can be reduced in 90 days without your agreement.

This clause is dangerous because it makes every other term in the contract conditional. A favorable fee schedule, a reasonable timely filing window, a fair recoupment policy: all of it can be rewritten unilaterally if this clause exists.

What to look for in your contract:

- Language granting the payer "sole discretion" to modify terms

- Notice periods shorter than 90 days

- Amendment delivery via website posting rather than direct written notice

- No requirement for provider consent or mutual agreement

What to negotiate instead: require mutual written consent for any material changes to the contract, especially fee schedules. If the payer insists on retaining amendment rights, negotiate a minimum 90-day notice period with a right to terminate without penalty if you reject the amendment.

The risk of a payer rewriting your rates at any time is serious. But some clauses let payers take back money you have already earned.

2. Unlimited recoupment windows let payers claw back payments from years ago

Recoupment clauses without a time limit allow payers to demand refunds on claims paid years, sometimes a decade, in the past. If the contract does not specify a recoupment window, the payer can audit old claims indefinitely and pull money from your current payments to offset alleged overpayments.

Dewey flags this as one of the most dangerous "trapdoors" in payer contracts, noting that some agreements allow clawbacks from claims filed as long as 10 years ago. DoctorsManagement confirms the pattern: "Periodically, physicians receive letters from payors or independent vendors requesting refunds for claims that were paid as long as three years ago."

The asymmetry is what makes this clause particularly harmful. When payers underpay a claim, providers face strict filing deadlines to appeal, often 60-90 days. When payers decide they overpaid, no equivalent deadline applies.

"I guarantee that if the insurance company would have overpaid us, Cigna would have pulled that money back a lot faster than a year."

- Scott Hurst, CEO of Patient Physician Network IPA (250 member practices, ~700 physicians)

What to look for in your contract:

- No stated time limit on recoupment or overpayment recovery

- Language allowing the payer to offset recoupments against current claim payments without notice

- Third-party audit provisions where an outside vendor initiates recoupment on the payer's behalf

What to negotiate instead: a reciprocal time limit (12-18 months is standard), a requirement for written notice and documentation before any recoupment, and a dispute resolution step before the payer can offset current payments. Many states also have anti-clawback statutes that override contract language, so check your state's provider protection laws.

Recoupment takes money you already earned. The next red flag prevents you from earning it in the first place.

3. Downcoding authority without clinical review reduces your payments automatically

Downcoding clauses grant the payer broad authority to reduce the level of a submitted claim based on claims data alone, without reviewing the patient's medical record. The claim gets paid at a lower level, but the billed code often remains unchanged in the system, making the underpayment invisible in standard coding audits.

"some contracts allow the payer to arbitrarily adjust claims and pay them at a lower level than submitted. A claims examiner may do the downcoding, or it may be done by rules-based software. In most cases the medical records aren't examined."

This practice drew sharp criticism from physicians when Cigna implemented a broad downcoding policy affecting E/M codes in 2025.

"A review basing an E/M downcode on claim information only 'is not a proper process' and 'should just go away.'"

- Dr. David Eagle, hematologist-oncologist, NY Cancer & Blood Specialists

"[Cigna's downcoding policy is] very, very heavy-handed... a real insult to physicians. They have no business dictating E/M levels."

- Dr. Join Y. Luh, radiation oncologist, Providence St. Joseph Health

What to look for in your contract:

- Vague references to "appropriate coding levels" or "industry standards" without defining who determines appropriateness

- Language granting the payer or its designee the right to "adjust" or "correct" claims

- No requirement for chart-based review before downcoding

- No defined appeals process for downcoded claims

What to negotiate instead: require medical record review before any claim adjustment, a defined peer-to-peer review process, and written notification with specific clinical rationale for every downcode.

Downcoding reduces what you get paid for services you already performed. A related tactic goes further: retroactively denying payment for services a payer already approved.

4. Prior authorization rescission and vague medical necessity definitions enable retroactive denials

Prior authorization rescission clauses allow a payer to revoke a prior authorization after the service has already been performed, leaving the provider with no reimbursement for care they delivered in good faith. Combined with vague medical necessity definitions, these clauses create a system where nearly any claim can be denied after the fact.

Dewey identifies prior authorization rescission as a specific contract "trapdoor" that physicians frequently overlook. The operational burden is already enormous. According to the AMA, around 80% of physicians report that prior authorization requirements rose over the past five years, and over 60% say it is difficult to even determine whether a service requires prior authorization.

The clinical consequences are not abstract. Dr. Fumiko Chino, a radiation oncologist at Memorial Sloan Kettering, described the stakes on the AMA Update podcast:

"I've seen patients die from prior authorization. I'll just put it like that. I'll be so bold."

When the contract language defines medical necessity in broad, subjective terms, it gives the payer a basis to deny virtually any claim retroactively. HOM RCM notes that undefined medical necessity criteria "enable retroactive denials" by leaving the standard entirely in the payer's hands.

What to look for in your contract:

- Any language allowing the payer to rescind, modify, or reverse a prior authorization after services have been rendered

- Medical necessity definitions that reference the payer's "sole discretion" or internal policies without specifying clinical criteria

- No requirement for peer-to-peer clinical review before a denial

What to negotiate instead: irrevocable prior authorization once granted (meaning the payer cannot rescind approval after you perform the service), medical necessity definitions tied to published clinical guidelines or specialty society standards, and mandatory peer-to-peer review with a board-certified physician in the relevant specialty before any denial.

These four red flags share a common pattern: you cannot detect them by looking at your fee schedule alone. The fifth red flag is about the fee schedule itself, and it requires a different kind of analysis.

5. Fee schedule opacity hides underpayment in plain sight

Contracts that reference fee schedules with vague terms like "usual and customary," "industry-accepted," or "percentage of Medicare" without specifying which year's schedule create a gap between expected and actual reimbursement that grows wider every year. Some contracts do not attach a full fee schedule at all, leaving the provider to guess what they agreed to be paid.

WebPT flags "industry-accepted" and "except as otherwise indicated herein" as specific red-flag phrases in payer contracts. When a contract says "110% of Medicare" but does not specify the fee schedule year, the payer can peg your rates to a 2019 schedule while you assume you are being paid based on the current year. The difference compounds annually.

This is where publicly available pricing data changes the equation. CMS now requires hospitals and payers to publish machine-readable files containing negotiated rates. That means providers can, for the first time, see what payers are actually paying other providers in their market for the same services.

How to benchmark your contracted rates:

- Pull the current CMS physician fee schedule for your top 10-15 CPT codes by volume

- Calculate your contracted rate as a percentage of Medicare for each code

- Compare against machine-readable file data from the same payer in your geographic area

- Identify codes where your contracted rate falls below what the payer is paying comparable providers

This analysis often reveals that a contract promising "competitive rates" is actually paying 15-20% below what the same payer pays a hospital-affiliated practice across town for identical services. According to AJMC, physician reimbursement has increased just 10% since 2001, while hospital payment has increased 70% over the same period. That disparity is baked into fee schedules, and it is only visible when you compare your rates against actual market data.

What to negotiate: explicit fee schedules attached to the contract as an exhibit, annual escalators tied to the CPI or the current-year Medicare fee schedule, and a defined methodology for rate calculations. If a payer resists attaching a fee schedule, that is itself a red flag.

What to do if you already signed a contract with these red flags

Most providers searching for payer contract red flags already have contracts in force. Identifying problems in an existing agreement is the first step. Monitoring for ongoing damage is the second.

Five actions to take on existing contracts:

- Pull every active payer contract into one location. Many practices store agreements across filing cabinets, email inboxes, and the memories of long-tenured staff. You cannot evaluate what you cannot find.

- Search each contract for the five red flags above. Use the "what to look for" checklists as a screening tool. Flag any contract containing unlimited recoupment, unilateral amendment rights, or vague fee schedule references.

- Track denial rates by payer monthly. A sudden spike in denials from one payer often signals a silent policy change or a unilateral amendment you were not notified about.

- Compare actual reimbursement against contracted rates quarterly. Match posted payments to your fee schedule at the CPT code level. This is the only way to catch silent underpayments and downcoding that does not change the billed code.

- Calendar your renegotiation windows. Evergreen contracts auto-renew if you miss the termination notice window, which locks you into another term under the same unfavorable terms. Set reminders 120 days before each renewal date.

Watch for payments from payers you do not have a direct contract with. This is the hallmark of silent PPO activity, where a third-party network leases your contracted rates to payers you never agreed to work with. According to Barta Law, a silent PPO "searches for the lowest discounted rate a physician has accepted with any insurance company and applies that discounted rate" to other payers' members, all without the physician's authorization or knowledge.

The leverage you did not have five years ago

Every red flag in this article shares one root cause: an information gap between payers and providers. Payers know exactly what they pay every provider in every market. Providers, historically, have not.

That gap is closing. CMS price transparency requirements now force payers to publish negotiated rates. Machine-readable files, while imperfect, give providers data they have never had before: what a payer actually pays for a given service, in a given market, across different provider types.

A contract review catches the clauses that are costing you money. Transparency data tells you whether the rates you agreed to were fair in the first place. Both are necessary. The providers who combine contract vigilance with market-rate benchmarking negotiate from data instead of hope. That is how you stop the quiet drain.

Share this article

Help spread the knowledge by sharing with others

Ready to see how your rates compare?

PayerPrice gives you instant access to negotiated rate data across payers and providers so you can benchmark, negotiate, and optimize with confidence.

Related Articles

Continue exploring healthcare transparency and compliance topics

How to Model a Payer Contract: A Provider's Guide

See how providers model payer contracts against real claims to catch a money-losing deal before signing. Formulas, a worked example, and a 5-step method.

How to Run Payer Contract Analytics (Physician Group Guide)

Stop signing stealth pay cuts. This guide shows physician groups how to benchmark rates, recover underpayments, and run payer contract analytics in-house.

How to Contract With Insurance Companies (Without a Bad Rate)

How to contract with insurance companies as a provider: the credentialing steps, the contract clauses to check, and how to tell if your rate is fair before you sign.